Array

(

[_wp_page_template] => Array

(

[0] => default

)

[_yoast_indexnow_last_ping] => Array

(

[0] => 1724397703

)

[_download_short_title] => Array

(

[0] => field_5cef892461912

)

[download_short_title] => Array

(

[0] => China Makeup Market Data Pack June 2020

)

[_download_intro] => Array

(

[0] => field_64ef2d5b76486

)

[download_intro] => Array

(

[0] => For this data pack series, TMO compiles data from Alibaba's family of eCommerce platforms (including Taobao, Tmall, Tmall Global, and Tmall Supermarket) regarding sales of Makeup both domestically and across borders. This data is presented in a form that's easier for English-speaking overseas companies and individuals to approach, with an array of charts and tables as well as translated terms. This special June edition covers top brand performance around the popular June 18th sales holiday.

)

[_download_preview_file] => Array

(

[0] => field_64edce2ff2e06

)

[download_preview_file] => Array

(

[0] =>

)

[_download_features] => Array

(

[0] => field_64edcc9a983cc

)

[download_features] => Array

(

[0] =>

)

[_download_related] => Array

(

[0] => field_5b39a37f8493b

)

[download_related] => Array

(

[0] =>

)

[_free_vs_premium] => Array

(

[0] => field_65b18a992edc6

)

[free_vs_premium] => Array

(

[0] =>

)

[_table_of_contents] => Array

(

[0] => field_65b18cc85d2c7

)

[table_of_contents] => Array

(

[0] =>

- Last month’s best-selling products

- Sub-category market share

- Market share by price range

- Top search keywords

- A spotlight on the most popular brands

- Best-selling product characteristics

- Best-selling products in each sub-category

- Best-selling products for each top brand

For more information, download the data pack today!

)

[_highlight] => Array

(

[0] => field_65b18d3a62844

)

[highlight] => Array

(

[0] => June has in recent years seen sales spikes across product categories, as the June 18th sales period has grown in popularity. Sales in fact often begin as early as June 1st, with brands jostling to be the first to tap into their consumers’ wallets. This June edition of the Data Pack therefore goes a little further in depth on leading brands and the June sales holiday in general.

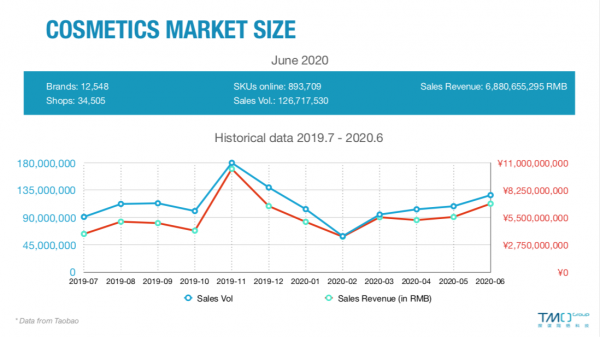

The CoViD-19 pandemic of early 2020 resulted in reduced sales for many product categories in China, but as the pandemic eased, we saw a trend of consumers 'treating themselves' as stores reopened and life returned to normal. This trend was particularly evident in the makeup market, a product category that is especially well-suited to personal pampering, with a strong rebound reaching peak sales for the year in June.

As the most populous country and the second largest economy in the world, China still maintains a strong stance after decades of rapid development. With the continuous increase of per capita disposable income, the Chinese market has undergone many consumption upgrades. Especially now, people’s pursuit of beauty has heated up the makeup market, surpassing the market in Japan from 2013 to become the second largest makeup market. It has also maintained a strong growth momentum in recent years.

Makeup consumption per capita in China is only about 1/4 of that in developed countries; the number of consumers is expected to reach 400 million in 2020; the sinking market and the rise of Generation Z in 2019 have also become another driving force for market growth.

Data shows that in 2019, the sales revenue from makeup is 55.2 billion yuan, which is only 22.5% of skincare products revenue. Experts expect that the revenue of the makeup industry will reach 124.3 billion yuan in 2024, which means that Chinese makeup market still has huge potential and entry opportunities. Many brands in recent years have proven this. New domestic brands such as Perfect Diary and Florasis became head brands in just a few years, while international brands like Kiko also achieved good results through cross-border eCommerce.

The publication of the new cosmetics management regulations also indicates the determination of Chinese government to create a healthy and sustainable industry. After the epidemic, we believe that the Chinese makeup industry will still maintain a gratifying growth rate, and the competition between brands will become fierce but increasingly transparent as well.

)

[_highlight_gallery] => Array

(

[0] => field_65b18d6f62845

)

[highlight_gallery] => Array

(

[0] => a:2:{i:0;s:5:"85632";i:1;s:5:"85633";}

)

[_highlight_popup] => Array

(

[0] => field_65b18d7f62846

)

[highlight_popup] => Array

(

[0] => 1

)

[_related_downloads] => Array

(

[0] => field_65b18dfcc580d

)

[related_downloads] => Array

(

[0] =>

)

[_banner_link_1] => Array

(

[0] => field_65b18eda3aab7

)

[banner_link_1] => Array

(

[0] => /contact/

)

[_banner_link_2] => Array

(

[0] => field_65b18f013aab8

)

[banner_link_2] => Array

(

[0] =>

)

[_qa] => Array

(

[0] => field_65b18f2c3aabb

)

[_qa_0_question] => Array

(

[0] => field_65b18f3b3aabc

)

[qa_0_question] => Array

(

[0] => Which payment methods are currently available to purchase a resource?

)

[_qa_0_answer] => Array

(

[0] => field_65b18f433aabd

)

[qa_0_answer] => Array

(

[0] => At the moment we only support credit card payments. However, in the near future this will be expanded to include other popular methods such as WeChat Pay and Alipay.

)

[_qa_1_question] => Array

(

[0] => field_65b18f3b3aabc

)

[qa_1_question] => Array

(

[0] => What should I do if I have not received my email or my payment failed?

)

[_qa_1_answer] => Array

(

[0] => field_65b18f433aabd

)

[qa_1_answer] => Array

(

[0] => If you encounter any problems throughout the ordering process, get in touch with us. You can reach us through our online customer service. Alternatively, you can send an email to info@tmogroup.asia or give us a call at +86 (0)21 617 00 396.

)

[_qa_2_question] => Array

(

[0] => field_65b18f3b3aabc

)

[qa_2_question] => Array

(

[0] => If my payment was successful, can I receive an invoice?

)

[_qa_2_answer] => Array

(

[0] => field_65b18f433aabd

)

[qa_2_answer] => Array

(

[0] => TMO Group can provide an invoice for purchase of the guides. If you need an invoice, please send a request by email to info@tmogroup.asia with the detailed company information for the invoice and the payment receipt. Once we receive, we can issue the digital invoice and send it to you via e-mail within 10 working days.

)

[qa] => Array

(

[0] => 4

)

[_edd_download_earnings] => Array

(

[0] => 0.000000

)

[_edd_download_sales] => Array

(

[0] => 47

)

[onesignal_meta_box_present] => Array

(

[0] => 1

)

[onesignal_send_notification] => Array

(

[0] =>

)

[onesignal_modify_title_and_content] => Array

(

[0] =>

)

[onesignal_notification_custom_heading] => Array

(

[0] =>

)

[onesignal_notification_custom_content] => Array

(

[0] =>

)

[_yoast_wpseo_focuskeywords] => Array

(

[0] => [{"keyword":"Makeup 618 data","score":39},{"keyword":"China Makeup market ","score":50},{"keyword":"China makeup 618","score":39}]

)

[_yoast_wpseo_keywordsynonyms] => Array

(

[0] => ["China makeup data","Makeup 618 2020 data","China cosmetics market","China cosmetics 618"]

)

[_yoast_wpseo_estimated-reading-time-minutes] => Array

(

[0] => 1

)

[_yoast_wpseo_wordproof_timestamp] => Array

(

[0] =>

)

[edd_price] => Array

(

[0] => 0.00

)

[edd_download_files] => Array

(

[0] => a:1:{i:1;a:6:{s:5:"index";s:1:"0";s:13:"attachment_id";s:1:"0";s:14:"thumbnail_size";s:5:"false";s:4:"name";s:21:"Makeup Data Pack June";s:4:"file";s:82:"https://www.tmogroup.asia/wp-content/uploads/edd/2020/07/Makeup-Data-Pack-June.pdf";s:9:"condition";s:3:"all";}}

)

[_edd_bundled_products] => Array

(

[0] => a:1:{i:0;s:1:"0";}

)

[_edd_button_behavior] => Array

(

[0] => add_to_cart

)

[download_intro_content_title] => Array

(

[0] => China Makeup Market Data Pack June 2020

)

[_download_intro_content_title] => Array

(

[0] => field_5cef892461912

)

[download_intro_content] => Array

(

[0] => For this data pack series, TMO compiles data from Alibaba's family of eCommerce platforms (including Taobao, Tmall, Tmall Global, and Tmall Supermarket) regarding sales of Makeup both domestically and across borders. This data is presented in a form that's easier for English-speaking overseas companies and individuals to approach, with an array of charts and tables as well as translated terms. This special June edition covers top brand performance around the popular June 18th sales holiday.

)

[_download_intro_content] => Array

(

[0] => field_5b39a9e1352d2

)

[related_section_title] => Array

(

[0] =>

)

[_related_section_title] => Array

(

[0] => field_5b3adde339f9b

)

[related_section_related_downloads_0_download] => Array

(

[0] => 47174

)

[_related_section_related_downloads_0_download] => Array

(

[0] => field_5b39a37f8493b

)

[related_section_related_downloads] => Array

(

[0] => 3

)

[_related_section_related_downloads] => Array

(

[0] => field_5b39a3138493a

)

[_edd_all_access_enabled] => Array

(

[0] =>

)

[_edd_all_access_settings] => Array

(

[0] =>

)

[_edd_all_access_receipt_settings] => Array

(

[0] =>

)

[_wp_old_date] => Array

(

[0] =>

)

[tmo_post_views_count] => Array

(

[0] => 2928

)

[inline_featured_image] => Array

(

[0] => 0

)

[otw_grid_manager_content] => Array

(

[0] => []

)

[_yoast_wpseo_focuskw] => Array

(

[0] => Makeup data

)

[_yoast_wpseo_metadesc] => Array

(

[0] => June 2020 report covers China makeup market stats, trends, changes in consumer demand, while touching on brand competitiveness and product characteristics.

)

[_yoast_wpseo_linkdex] => Array

(

[0] => 37

)

[download_description_0_title] => Array

(

[0] =>

)

[_download_description_0_title] => Array

(

[0] => field_5b399a5d21e4c

)

[download_description_0_content] => Array

(

[0] =>

.

June has in recent years seen sales spikes across product categories, as the June 18th sales period has grown in popularity. Sales in fact often begin as early as June 1st, with brands jostling to be the first to tap into their consumers’ wallets. This June edition of the Data Pack therefore goes a little further in depth on leading brands and the June sales holiday in general.

The CoViD-19 pandemic of early 2020 resulted in reduced sales for many product categories in China, but as the pandemic eased, we saw a trend of consumers 'treating themselves' as stores reopened and life returned to normal. This trend was particularly evident in the makeup market, a product category that is especially well-suited to personal pampering, with a strong rebound reaching peak sales for the year in June.

As the most populous country and the second largest economy in the world, China still maintains a strong stance after decades of rapid development. With the continuous increase of per capita disposable income, the Chinese market has undergone many consumption upgrades. Especially now, people’s pursuit of beauty has heated up the makeup market, surpassing the market in Japan from 2013 to become the second largest makeup market. It has also maintained a strong growth momentum in recent years.

Makeup consumption per capita in China is only about 1/4 of that in developed countries; the number of consumers is expected to reach 400 million in 2020; the sinking market and the rise of Generation Z in 2019 have also become another driving force for market growth.

Data shows that in 2019, the sales revenue from makeup is 55.2 billion yuan, which is only 22.5% of skincare products revenue. Experts expect that the revenue of the makeup industry will reach 124.3 billion yuan in 2024, which means that Chinese makeup market still has huge potential and entry opportunities. Many brands in recent years have proven this. New domestic brands such as Perfect Diary and Florasis became head brands in just a few years, while international brands like Kiko also achieved good results through cross-border eCommerce.

The publication of the new cosmetics management regulations also indicates the determination of Chinese government to create a healthy and sustainable industry. After the epidemic, we believe that the Chinese makeup industry will still maintain a gratifying growth rate, and the competition between brands will become fierce but increasingly transparent as well.

)

[_download_description_0_content] => Array

(

[0] => field_5b399a6b21e4d

)

[download_description_1_title] => Array

(

[0] =>

)

[_download_description_1_title] => Array

(

[0] =>

)

[download_description_1_content] => Array

(

[0] =>

)

[_download_description_1_content] => Array

(

[0] =>

)

[download_description_2_title] => Array

(

[0] => Who are these data packs intended for?

)

[_download_description_2_title] => Array

(

[0] => field_5b399a5d21e4c

)

[download_description_2_content] => Array

(

[0] => These data packs are designed to assist researchers, data analysts, product development professionals, business decision makers, and anyone involved in strategic planning at overseas Makeup companies, or entities or individuals interested in this area. By keeping up with each month's shifts in sales and consumer behavior, such experts can get a more firm grip on the trends and shifting attitudes in China's growing and increasingly competitive Makeup market.

)

[_download_description_2_content] => Array

(

[0] => field_5b399a6b21e4d

)

[related_section_related_downloads_1_download] => Array

(

[0] => 50408

)

[_related_section_related_downloads_1_download] => Array

(

[0] => field_5b39a37f8493b

)

[related_section_related_downloads_2_download] => Array

(

[0] => 40838

)

[_related_section_related_downloads_2_download] => Array

(

[0] => field_5b39a37f8493b

)

[_yoast_wpseo_primary_download_category] => Array

(

[0] => 154

)

[_edd_download_limit_override_41775] => Array

(

[0] =>

)

[_wp_old_slug] => Array

(

[0] =>

[1] => china-makeup-market-data-pack-june-2020-2

)

[_dp_original] => Array

(

[0] =>

)

[download_description_3_title] => Array

(

[0] => This data pack includes:

)

[_download_description_3_title] => Array

(

[0] => field_5b399a5d21e4c

)

[download_description_3_content] => Array

(

[0] =>

- Last month's best-selling products

- Sub-category market share

- Market share by price range

- Top search keywords

- Most popular brands

- Best-selling product characteristics

- Best-selling products in each sub-category

- Best-selling products for each top brand

And more!

Subscribe to our monthly data pack to download today!

)

[_download_description_3_content] => Array

(

[0] => field_5b399a6b21e4d

)

[download_description_4_image_row_0_image] => Array

(

[0] => 40013

)

[_download_description_4_image_row_0_image] => Array

(

[0] => field_5b39a07f6cde0

)

[download_description_4_image_row_0_lightbox] => Array

(

[0] => 1

)

[_download_description_4_image_row_0_lightbox] => Array

(

[0] => field_5b5947836e6c1

)

[download_description_4_image_row_0_gallery] => Array

(

[0] => a:1:{i:0;s:5:"40013";}

)

[_download_description_4_image_row_0_gallery] => Array

(

[0] => field_5b5947a86e6c2

)

[download_description_4_image_row_0_row_id] => Array

(

[0] => 5f0c1b040e202

)

[_download_description_4_image_row_0_row_id] => Array

(

[0] => field_5b5947ce6e6c3

)

[download_description_4_image_row_1_image] => Array

(

[0] => 40014

)

[_download_description_4_image_row_1_image] => Array

(

[0] => field_5b39a07f6cde0

)

[download_description_4_image_row_1_lightbox] => Array

(

[0] => 1

)

[_download_description_4_image_row_1_lightbox] => Array

(

[0] => field_5b5947836e6c1

)

[download_description_4_image_row_1_gallery] => Array

(

[0] => a:1:{i:0;s:5:"40014";}

)

[_download_description_4_image_row_1_gallery] => Array

(

[0] => field_5b5947a86e6c2

)

[download_description_4_image_row_1_row_id] => Array

(

[0] => 5f0c1b0416c75

)

[_download_description_4_image_row_1_row_id] => Array

(

[0] => field_5b5947ce6e6c3

)

[download_description_4_image_row] => Array

(

[0] => 2

)

[_download_description_4_image_row] => Array

(

[0] => field_5b39a0486cddf

)

[download_description_4_title] => Array

(

[0] =>

)

[_download_description_4_title] => Array

(

[0] =>

)

[download_description_4_content] => Array

(

[0] =>

)

[_download_description_4_content] => Array

(

[0] =>

)

[download_description_6_image_row_0_image] => Array

(

[0] =>

)

[_download_description_6_image_row_0_image] => Array

(

[0] =>

)

[download_description_6_image_row_0_lightbox] => Array

(

[0] =>

)

[_download_description_6_image_row_0_lightbox] => Array

(

[0] =>

)

[download_description_6_image_row_0_gallery] => Array

(

[0] =>

)

[_download_description_6_image_row_0_gallery] => Array

(

[0] =>

)

[download_description_6_image_row_0_row_id] => Array

(

[0] =>

)

[_download_description_6_image_row_0_row_id] => Array

(

[0] =>

)

[download_description_6_image_row_1_image] => Array

(

[0] =>

)

[_download_description_6_image_row_1_image] => Array

(

[0] =>

)

[download_description_6_image_row_1_lightbox] => Array

(

[0] =>

)

[_download_description_6_image_row_1_lightbox] => Array

(

[0] =>

)

[download_description_6_image_row_1_gallery] => Array

(

[0] =>

)

[_download_description_6_image_row_1_gallery] => Array

(

[0] =>

)

[download_description_6_image_row_1_row_id] => Array

(

[0] =>

)

[_download_description_6_image_row_1_row_id] => Array

(

[0] =>

)

[download_description_6_image_row] => Array

(

[0] =>

)

[_download_description_6_image_row] => Array

(

[0] =>

)

[download_description_2_image_row_0_image] => Array

(

[0] =>

)

[_download_description_2_image_row_0_image] => Array

(

[0] =>

)

[download_description_2_image_row_0_lightbox] => Array

(

[0] =>

)

[_download_description_2_image_row_0_lightbox] => Array

(

[0] =>

)

[download_description_2_image_row_0_gallery] => Array

(

[0] =>

)

[_download_description_2_image_row_0_gallery] => Array

(

[0] =>

)

[download_description_2_image_row_0_row_id] => Array

(

[0] =>

)

[_download_description_2_image_row_0_row_id] => Array

(

[0] =>

)

[download_description_2_image_row_1_image] => Array

(

[0] =>

)

[_download_description_2_image_row_1_image] => Array

(

[0] =>

)

[download_description_2_image_row_1_lightbox] => Array

(

[0] =>

)

[_download_description_2_image_row_1_lightbox] => Array

(

[0] =>

)

[download_description_2_image_row_1_gallery] => Array

(

[0] =>

)

[_download_description_2_image_row_1_gallery] => Array

(

[0] =>

)

[download_description_2_image_row_1_row_id] => Array

(

[0] =>

)

[_download_description_2_image_row_1_row_id] => Array

(

[0] =>

)

[download_description_2_image_row] => Array

(

[0] =>

)

[_download_description_2_image_row] => Array

(

[0] =>

)

[download_description_5_title] => Array

(

[0] =>

)

[_download_description_5_title] => Array

(

[0] =>

)

[download_description_5_content] => Array

(

[0] =>

)

[_download_description_5_content] => Array

(

[0] =>

)

[download_description_8_title] => Array

(

[0] =>

)

[_download_description_8_title] => Array

(

[0] =>

)

[download_description_8_content] => Array

(

[0] =>

)

[_download_description_8_content] => Array

(

[0] =>

)

[download_description_9_title] => Array

(

[0] =>

)

[_download_description_9_title] => Array

(

[0] =>

)

[download_description_9_content] => Array

(

[0] =>

)

[_download_description_9_content] => Array

(

[0] =>

)

[download_description_3_image_row_0_image] => Array

(

[0] =>

)

[_download_description_3_image_row_0_image] => Array

(

[0] =>

)

[download_description_3_image_row_0_lightbox] => Array

(

[0] =>

)

[_download_description_3_image_row_0_lightbox] => Array

(

[0] =>

)

[download_description_3_image_row_0_gallery] => Array

(

[0] =>

)

[_download_description_3_image_row_0_gallery] => Array

(

[0] =>

)

[download_description_3_image_row_0_row_id] => Array

(

[0] =>

)

[_download_description_3_image_row_0_row_id] => Array

(

[0] =>

)

[download_description_3_image_row_1_image] => Array

(

[0] =>

)

[_download_description_3_image_row_1_image] => Array

(

[0] =>

)

[download_description_3_image_row_1_lightbox] => Array

(

[0] =>

)

[_download_description_3_image_row_1_lightbox] => Array

(

[0] =>

)

[download_description_3_image_row_1_gallery] => Array

(

[0] =>

)

[_download_description_3_image_row_1_gallery] => Array

(

[0] =>

)

[download_description_3_image_row_1_row_id] => Array

(

[0] =>

)

[_download_description_3_image_row_1_row_id] => Array

(

[0] =>

)

[download_description_3_image_row] => Array

(

[0] =>

)

[_download_description_3_image_row] => Array

(

[0] =>

)

[download_description_6_title] => Array

(

[0] =>

)

[_download_description_6_title] => Array

(

[0] =>

)

[download_description_6_content] => Array

(

[0] =>

)

[_download_description_6_content] => Array

(

[0] =>

)

[download_description_5_image_row_0_image] => Array

(

[0] =>

)

[_download_description_5_image_row_0_image] => Array

(

[0] =>

)

[download_description_5_image_row_0_lightbox] => Array

(

[0] =>

)

[_download_description_5_image_row_0_lightbox] => Array

(

[0] =>

)

[download_description_5_image_row_0_gallery] => Array

(

[0] =>

)

[_download_description_5_image_row_0_gallery] => Array

(

[0] =>

)

[download_description_5_image_row_0_row_id] => Array

(

[0] =>

)

[_download_description_5_image_row_0_row_id] => Array

(

[0] =>

)

[download_description_5_image_row_1_image] => Array

(

[0] =>

)

[_download_description_5_image_row_1_image] => Array

(

[0] =>

)

[download_description_5_image_row_1_lightbox] => Array

(

[0] =>

)

[_download_description_5_image_row_1_lightbox] => Array

(

[0] =>

)

[download_description_5_image_row] => Array

(

[0] =>

)

[_download_description_5_image_row] => Array

(

[0] =>

)

[download_description_7_title] => Array

(

[0] =>

)

[_download_description_7_title] => Array

(

[0] =>

)

[download_description_7_content] => Array

(

[0] =>

)

[_download_description_7_content] => Array

(

[0] =>

)

[download_description_7_image_row_0_image] => Array

(

[0] =>

)

[_download_description_7_image_row_0_image] => Array

(

[0] =>

)

[download_description_7_image_row_0_lightbox] => Array

(

[0] =>

)

[_download_description_7_image_row_0_lightbox] => Array

(

[0] =>

)

[download_description_7_image_row_0_gallery] => Array

(

[0] =>

)

[_download_description_7_image_row_0_gallery] => Array

(

[0] =>

)

[download_description_7_image_row_0_row_id] => Array

(

[0] =>

)

[_download_description_7_image_row_0_row_id] => Array

(

[0] =>

)

[download_description_7_image_row_1_image] => Array

(

[0] =>

)

[_download_description_7_image_row_1_image] => Array

(

[0] =>

)

[download_description_7_image_row_1_lightbox] => Array

(

[0] =>

)

[_download_description_7_image_row_1_lightbox] => Array

(

[0] =>

)

[download_description_7_image_row_1_gallery] => Array

(

[0] =>

)

[_download_description_7_image_row_1_gallery] => Array

(

[0] =>

)

[download_description_7_image_row_1_row_id] => Array

(

[0] =>

)

[_download_description_7_image_row_1_row_id] => Array

(

[0] =>

)

[download_description_7_image_row] => Array

(

[0] =>

)

[_download_description_7_image_row] => Array

(

[0] =>

)

[download_description_9_image_row_0_image] => Array

(

[0] =>

)

[_download_description_9_image_row_0_image] => Array

(

[0] =>

)

[download_description_9_image_row_0_lightbox] => Array

(

[0] =>

)

[_download_description_9_image_row_0_lightbox] => Array

(

[0] =>

)

[download_description_9_image_row_0_gallery] => Array

(

[0] =>

)

[_download_description_9_image_row_0_gallery] => Array

(

[0] =>

)

[download_description_9_image_row_0_row_id] => Array

(

[0] =>

)

[_download_description_9_image_row_0_row_id] => Array

(

[0] =>

)

[download_description_9_image_row_1_image] => Array

(

[0] =>

)

[_download_description_9_image_row_1_image] => Array

(

[0] =>

)

[download_description_9_image_row_1_lightbox] => Array

(

[0] =>

)

[_download_description_9_image_row_1_lightbox] => Array

(

[0] =>

)

[download_description_9_image_row_1_gallery] => Array

(

[0] =>

)

[_download_description_9_image_row_1_gallery] => Array

(

[0] =>

)

[download_description_9_image_row_1_row_id] => Array

(

[0] =>

)

[_download_description_9_image_row_1_row_id] => Array

(

[0] =>

)

[download_description_9_image_row] => Array

(

[0] =>

)

[_download_description_9_image_row] => Array

(

[0] =>

)

[_edd_download_limit_override_56532] => Array

(

[0] =>

)

[download_description_5_image_row_1_gallery] => Array

(

[0] =>

)

[_download_description_5_image_row_1_gallery] => Array

(

[0] =>

)

[download_description_5_image_row_1_row_id] => Array

(

[0] =>

)

[_download_description_5_image_row_1_row_id] => Array

(

[0] =>

)

[_edd_download_limit_override_63320] => Array

(

[0] =>

)

[_edd_download_limit_override_63318] => Array

(

[0] =>

)

[mmpm_post_icon] => Array

(

[0] =>

)

[_edd_download_limit_override_40494] => Array

(

[0] =>

)

[download_intro_title] => Array

(

[0] =>

)

[_download_intro_title] => Array

(

[0] =>

)

[_yoast_wpseo_focuskw_text_input] => Array

(

[0] =>

)

[download_description_1_image_row_0_image] => Array

(

[0] =>

)

[_download_description_1_image_row_0_image] => Array

(

[0] =>

)

[download_description_1_image_row_1_image] => Array

(

[0] =>

)

[_download_description_1_image_row_1_image] => Array

(

[0] =>

)

[download_description_1_image_row] => Array

(

[0] =>

)

[_download_description_1_image_row] => Array

(

[0] =>

)

[download_description_1_image_row_0_lightbox] => Array

(

[0] =>

)

[_download_description_1_image_row_0_lightbox] => Array

(

[0] =>

)

[download_description_1_image_row_0_gallery] => Array

(

[0] =>

)

[_download_description_1_image_row_0_gallery] => Array

(

[0] =>

)

[download_description_1_image_row_0_row_id] => Array

(

[0] =>

)

[_download_description_1_image_row_0_row_id] => Array

(

[0] =>

)

[download_description_1_image_row_1_lightbox] => Array

(

[0] =>

)

[_download_description_1_image_row_1_lightbox] => Array

(

[0] =>

)

[download_description_1_image_row_1_gallery] => Array

(

[0] =>

)

[_download_description_1_image_row_1_gallery] => Array

(

[0] =>

)

[download_description_1_image_row_1_row_id] => Array

(

[0] =>

)

[_download_description_1_image_row_1_row_id] => Array

(

[0] =>

)

[_edd_download_limit_override_34805] => Array

(

[0] =>

)

[_edd_download_limit_override_35321] => Array

(

[0] =>

)

[_edd_download_limit_override_40045] => Array

(

[0] =>

)

[_edd_download_limit_override_63326] => Array

(

[0] =>

)

[_edd_download_limit_override_37055] => Array

(

[0] =>

)

[_edd_download_limit_override_53159] => Array

(

[0] =>

)

[_edd_download_limit_override_53189] => Array

(

[0] =>

)

[edd_sku] => Array

(

[0] =>

)

[_edd_download_limit_override_37509] => Array

(

[0] =>

)

[_edd_download_limit_override_55976] => Array

(

[0] =>

)

[_edd_download_limit_override_63328] => Array

(

[0] =>

)

[_edd_download_limit_override_63322] => Array

(

[0] =>

)

[_edd_download_limit_override_41767] => Array

(

[0] =>

)

[_edd_download_limit_override_54353] => Array

(

[0] =>

)

[_edd_download_limit_override_39021] => Array

(

[0] =>

)

[_edd_download_limit_override_53193] => Array

(

[0] =>

)

[_edd_download_limit_override_63332] => Array

(

[0] =>

)

[download_description_1_image_row_2_image] => Array

(

[0] =>

)

[_download_description_1_image_row_2_image] => Array

(

[0] =>

)

[download_description_1_image_row_2_lightbox] => Array

(

[0] =>

)

[_download_description_1_image_row_2_lightbox] => Array

(

[0] =>

)

[download_description_1_image_row_2_gallery] => Array

(

[0] =>

)

[_download_description_1_image_row_2_gallery] => Array

(

[0] =>

)

[download_description_1_image_row_2_row_id] => Array

(

[0] =>

)

[_download_description_1_image_row_2_row_id] => Array

(

[0] =>

)

[download_description_4_image_row_2_image] => Array

(

[0] =>

)

[_download_description_4_image_row_2_image] => Array

(

[0] =>

)

[download_description_4_image_row_2_lightbox] => Array

(

[0] =>

)

[_download_description_4_image_row_2_lightbox] => Array

(

[0] =>

)

[download_description_4_image_row_2_gallery] => Array

(

[0] =>

)

[_download_description_4_image_row_2_gallery] => Array

(

[0] =>

)

[download_description_4_image_row_2_row_id] => Array

(

[0] =>

)

[_download_description_4_image_row_2_row_id] => Array

(

[0] =>

)

[download_description_10_title] => Array

(

[0] =>

)

[_download_description_10_title] => Array

(

[0] =>

)

[download_description_10_content] => Array

(

[0] =>

)

[_download_description_10_content] => Array

(

[0] =>

)

[_thumbnail_id] => Array

(

[0] => 85206

)

[_edit_lock] => Array

(

[0] => 1724397717:7

)

[_edit_last] => Array

(

[0] => 7

)

[download_thumbnail] => Array

(

[0] => 85326

)

[_download_thumbnail] => Array

(

[0] => field_65dfe4f92ef0e

)

[page_link] => Array

(

[0] =>

)

[_page_link] => Array

(

[0] => field_65de8afb998f5

)

[free_download] => Array

(

[0] =>

)

[_free_download] => Array

(

[0] => field_65c434b88abef

)

[companies] => Array

(

[0] => a:16:{i:0;s:5:"87064";i:1;s:5:"87067";i:2;s:5:"87071";i:3;s:5:"87074";i:4;s:5:"87070";i:5;s:5:"87078";i:6;s:5:"87076";i:7;s:5:"87075";i:8;s:5:"87077";i:9;s:5:"87072";i:10;s:5:"87079";i:11;s:5:"87101";i:12;s:5:"87102";i:13;s:5:"87065";i:14;s:5:"87073";i:15;s:5:"87068";}

)

[_companies] => Array

(

[0] => field_65e5bd0a33aac

)

[_ct_other_template] => Array

(

[0] => 0

)

[_ct_template_archive_post_types_all] => Array

(

[0] =>

)

[_ct_template_categories] => Array

(

[0] => a:0:{}

)

[_ct_template_categories_all] => Array

(

[0] =>

)

[_ct_template_tags] => Array

(

[0] => a:0:{}

)

[_ct_template_tags_all] => Array

(

[0] =>

)

[_ct_template_custom_taxonomies] => Array

(

[0] => a:0:{}

)

[_ct_template_custom_taxonomies_all] => Array

(

[0] =>

)

[_ct_template_authors_archives_all] => Array

(

[0] =>

)

[_ct_template_index] => Array

(

[0] =>

)

[_ct_template_front_page] => Array

(

[0] =>

)

[_ct_template_blog_posts] => Array

(

[0] =>

)

[_ct_template_date_archive] => Array

(

[0] =>

)

[_ct_template_search_page] => Array

(

[0] =>

)

[_ct_template_inner_content] => Array

(

[0] =>

)

[_ct_template_404_page] => Array

(

[0] =>

)

[_ct_template_all_archives] => Array

(

[0] =>

)

[_ct_template_archive_among_taxonomies] => Array

(

[0] => a:0:{}

)

[_ct_template_apply_if_archive_among_taxonomies] => Array

(

[0] =>

)

[_ct_template_archive_post_types] => Array

(

[0] => a:0:{}

)

[_ct_template_apply_if_archive_among_cpt] => Array

(

[0] =>

)

[_ct_template_authors_archives] => Array

(

[0] => a:0:{}

)

[_ct_template_apply_if_archive_among_authors] => Array

(

[0] =>

)

[_ct_template_single_all] => Array

(

[0] =>

)

[_ct_template_post_types] => Array

(

[0] => a:0:{}

)

[_ct_template_exclude_ids] => Array

(

[0] =>

)

[_ct_template_include_ids] => Array

(

[0] =>

)

[_ct_template_taxonomies] => Array

(

[0] => a:2:{s:5:"names";a:0:{}s:6:"values";a:0:{}}

)

[_ct_use_template_taxonomies] => Array

(

[0] =>

)

[_ct_template_post_of_parents] => Array

(

[0] => a:0:{}

)

[_ct_template_apply_if_post_of_parents] => Array

(

[0] =>

)

[_ct_template_order] => Array

(

[0] => 0

)

[_ct_builder_shortcodes] => Array

(

[0] =>

)

[_oxygen_lock_post_edit_mode] => Array

(

[0] =>

)

[_a3_pvc_activated] => Array

(

[0] => false

)

[button_link] => Array

(

[0] =>

)

[_button_link] => Array

(

[0] => field_65de8afb998f5

)

[cmplz_hide_cookiebanner] => Array

(

[0] =>

)

[_edd_download_gross_sales] => Array

(

[0] => 47

)

[_edd_download_gross_earnings] => Array

(

[0] => 0

)

[_qa_3_question] => Array

(

[0] => field_65b18f3b3aabc

)

[qa_3_question] => Array

(

[0] => I need specific data about my industry, do you offer customized reports?

)

[_qa_3_answer] => Array

(

[0] => field_65b18f433aabd

)

[qa_3_answer] => Array

(

[0] => Yes! From preliminary eCommerce scans that inform your market entry strategy, to monthly data checks, and long-term monitoring, we offer custom data collection and analysis to help identify your industry's market structure, pricing, top competitors, trends, and more. To learn more, navigate to our "Data Service" page in the main menu or contact us to discuss your data needs.

)

[_banner_title] => Array

(

[0] => field_6650573688572

)

[banner_title] => Array

(

[0] => Need specific data for your business?

)

[_button_text] => Array

(

[0] => field_6650576288573

)

[button_text] => Array

(

[0] => Customize your report

)

)