It’s never been easier to sell to China from abroad than now. With cross-border eCommerce imports surpassing ¥500 billion in 2023, the surge in global brands entering the market reflects not only China’s growing middle class but also the government’s efforts to streamline cross-border processes for foreign merchants.

However, foreign brands still face challenges such as navigating import regulations, taxation, and delivery expectations in an increasingly competitive environment.

One particularly convenient and cost-effective solution for entering the Chinese Market is Bonded Warehousing, a model that helps businesses optimize their logistics, reduce taxes, and enhance delivery times. In this article, we’ll break down how bonded warehousing works and its role in helping foreign brands succeed in the Chinese market.

TMO specializes in China CBEC Solutions to help foreign brands establish a legal presence and develop winning go-to-market strategies.

China Logistics Infrastructure

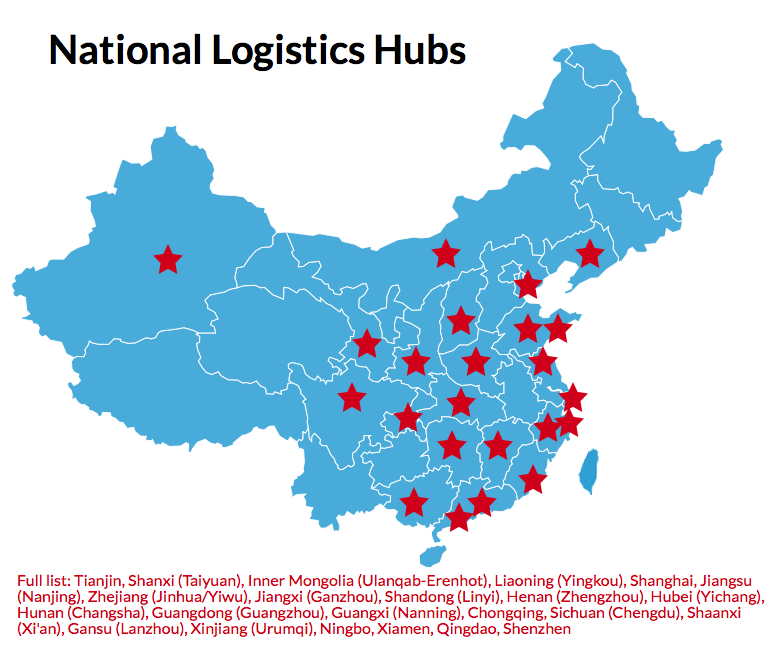

China’s logistics infrastructure has developed rapidly, with the number of National Logistic Hubs expected to reach 150 by 2025. This is part of China’s broader effort to support the expansion of cross-border eCommerce, which has grown by more than 10x over the past five years, according to the People’s Daily.

Foreign merchants hoping to sell to China today must be aware that Chinese consumers have grown accustomed to and expect reliable and quick delivery. Particularly in tier-one cities, products are more and more likely to be delivered within 24 hours. Growing networks of city warehouses and advances in logistic technologies made it a norm for popular items to be delivered within hours.

Getting your goods from A to B in China is no longer very difficult. It is, however, quite challenging to find the most optimal logistics solution to serve your Chinese consumers, as well as figuring out things like import licenses, product registrations, and customs regulations.

The Positive List: What can be imported via CBEC?

In China, not all products can be imported to China without restrictions. The Positive List is a government-approved list of 1,476 product categories that are eligible for import under a cross-border eCommerce model. This list is critical for businesses looking to sell to China, as products not on the list are subject to stricter import requirements and taxes.

Ensure your products qualify for cross-border eCommerce by consulting the latest version of the Positive List, revised in 2022.

Additionally to the Positive List, only goods with HS codes can be imported and sold via CBEC, whereas all other goods must be imported under the general trade model. Direct Selling is also possible for products from the Positive List, so they can alternatively be shipped from an overseas distribution center linked to Chinese customs without applying for an import license or an import certificate.

Import Models: Your Options for Entering the Chinese Market

When it comes to importing products into China through cross-border eCommerce, there are two primary models: Bonded Imports and Direct Purchase Imports. Below, we’ll outline these two models and how they impact your business.

For a breakdown of the benefits and challenges of each model, also read our article: China CBEC: Bonded Warehouse vs Direct Shipping ModelsDifferences, benefits, and challenges of Direct Shipping & Bonded Zone logistics models for overseas brands doing cross-border eCommerce in China.China Cross-border eCommerce: Bonded Warehouse vs Direct Mail Model (opens in a new tab)

1. Bonded Imports:

This import model can be further divided into two categories:

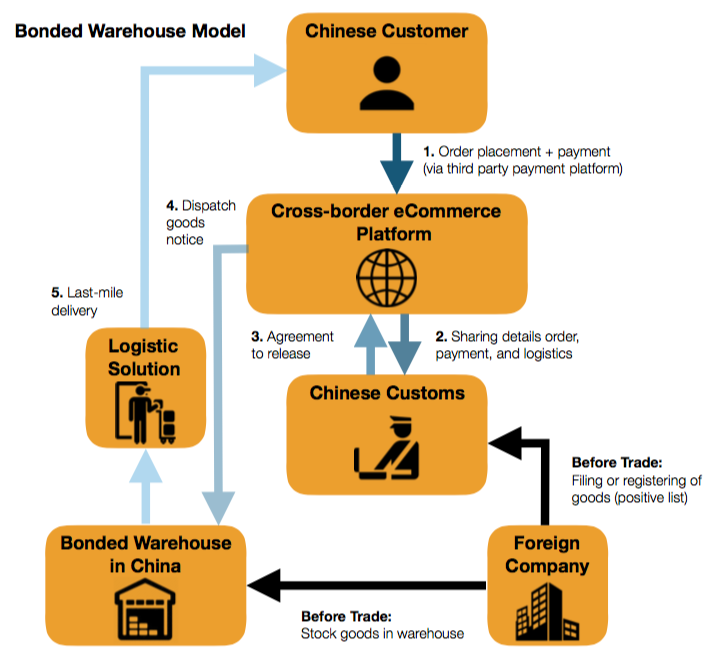

- Bonded Warehouse Model: Products are imported in bulk into approved bonded warehouse zones in China. Customs clearance is done after consumers place an order on a registered platform. Key benefits include postponed import duties and VAT until the sale is made, quicker delivery times, and simplified customs procedures.

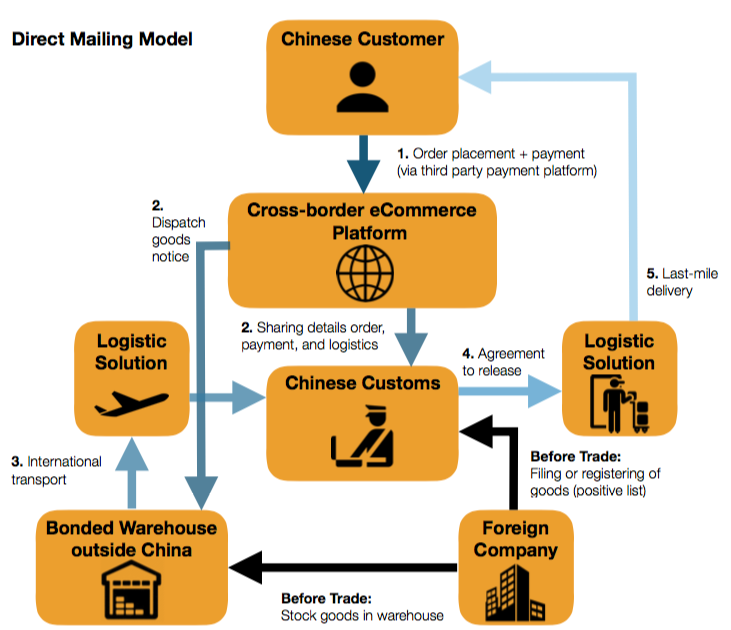

- Direct Mailing Model: In this model, individual orders are placed by consumers first on registered CBEC platforms, which in turn will submit the records of the order, shipment, and payment. Once products are shipped directly from overseas warehouses, they will pass through Customs more efficiently and be taken for last-mile delivery.

2. Direct Purchase Imports:

Under the Direct Purchase Import model, goods are shipped directly to the consumer from an overseas location after the order is placed, and follows a similar process to the direct mailing model, although it applies to products that are not included on the Positive List and comes with higher tax burdens, product registration, and consequently slower delivery times.

Not sure which import model is best for your China Market Entry project? Reach out to us to develop your China Cross-border eCommerce strategy.

The CBEC Bonded Warehousing Approach

Cross-border eCommerce started mainly via sales of Chinese individuals living abroad, and offering foreign products on marketplaces such as Taobao. In response to the outburst of these semi-legal cross-border shipments from overseas individuals, the Chinese government assigned 6 cross-border eCommerce comprehensive pilot cities in 2012. These comprehensive pilot zones are designated areas—generally near large trading ports—that provide a favorable business environment and infrastructure for cross-border eCommerce. The main feature of these pilot zones is the so-called bonded warehouses.

A bonded warehouse is a building or secured area in a special customs supervision area in China in which dutiable goods are stored before payment of duties. This usually ensures products arrive much more quickly.

As of 2023, there are 165 approved pilot zones, with the latest wave being announced in late 2022:

The main benefits that make bonded warehousing an attractive approach for businesses looking to enter the market efficiently and cost-effectively are:

- Postponed Payment of Duties and Taxes: Import duties and VAT are deferred until the product is sold to the consumer, helping businesses improve cash flow and reduce upfront costs.

- Faster Delivery Times: Goods are stored in bonded warehouses within China’s cross-border eCommerce zones, meaning they are already in the country and can be delivered quickly to consumers once an order is placed.

- Simplified Customs Clearance: Products stored in bonded warehouses benefit from expedited customs processes, as goods are pre-cleared when they arrive in bulk, with final clearance happening only when an order is placed.

- Lower Regulatory Barriers: Foreign businesses can bypass many of the strict import license and product registration requirements that apply to traditional import models.

- Enhanced Scalability: The ability to import products in bulk and store them domestically in China enables businesses to scale more efficiently. It also helps manage supply chain disruptions by having goods readily available in the market.

Recent Cross-border eCommerce Reforms

The Chinese government recognizes cross-border eCommerce as a special import channel, and has made several important updates to cross-border eCommerce regulations in recent years, particularly in terms of taxation and the scope of products eligible for bonded warehousing.

Key reforms from the Ministry of Finance, General Administration of Customs, and the General Administration of Taxation include:

- Tax Thresholds: Products valued under RMB 5,000 per transaction or RMB 26,000 annually per individual can benefit from reduced VAT (30% off the normal rate) and are exempt from import duties. If Customs is unable to access the electronic information of goods imported through CBEC, they will be subject to new parcel tax rates (currently standing at 13%, 20%, and 50%) with exemptions still available for payable tax amounts below RMB 50.

- Customs Procedures: The Chinese authorities have simplified customs procedures for cross-border eCommerce transactions, allowing for faster processing of bonded warehouse goods.

- Expanded Product Categories: The Positive List was updated in 2022 to include 29 additional product categories, making it easier for foreign businesses to enter the market.

Keep your business compliant with China’s latest reforms by exploring our China Digital Compliance Services and staying up to date with the latest regulations.

Designing a Winning CBEC Strategy with TMO

The opportunities in China’s cross-border eCommerce market are vast, but success requires the right strategy. Bonded warehousing is just one of the many tools you can use to streamline your operations, reduce taxes, and deliver faster to consumers. At TMO Group, we specialize in helping businesses navigate the complexities of China’s cross-border eCommerce market. From establishing a legal presence in China to handling customs pre-filing and product feasibility studies, we offer tailored solutions to ensure your success.

Whether you’re looking to set up a bonded warehouse approach or simply optimize your existing strategy, we can help you design a compliant, efficient Go-to-Market plan. Our expertise spans across various business models, including B2B and distribution, making us the perfect partner for your China market entry.

Contact us today for a custom proposal that addresses your unique needs and helps you navigate the evolving landscape of China’s cross-border eCommerce!

You may also be interested in this article about warehousing and storage services in China from our our partner Sino Shipping.